Combining Merchant Services and Payroll for Maximum Efficiency

Charles Bayani

April 13, 2026

Combined merchant services and payroll consolidates your payment processing and employee compensation into a single platform, eliminating the reconciliation burden, duplicate data entry, and multiple vendor fees that drain small business resources. Businesses managing separate merchant services and payroll systems typically spend 5 to 10 additional hours per month on reconciliation and pay 15% to 25% more in combined fees than those using a unified payment solution. We provide all-in-one payment and payroll platforms designed for small businesses that want one dashboard, one support team, and one monthly statement. This guide compares the separate versus integrated model, breaks down the cost savings, and outlines what to evaluate when choosing a unified platform.

The Problem With Separate Systems

Operating merchant services and payroll through different providers creates three friction points that compound as your business grows: data fragmentation, reconciliation overhead, and fee duplication.

Data fragmentation means your revenue data lives in one system while your labor costs live in another. Generating a real-time profit margin requires manually exporting from both platforms, aligning time periods, and reconciling discrepancies. For businesses processing $50,000+ in monthly card transactions with 10+ employees, this fragmentation consumes hours that produce zero revenue.

Reconciliation overhead emerges every pay period and every month-end. Your bookkeeper or accountant must match payment deposits to merchant batches, verify processing fees against statements, calculate payroll tax withholdings, reconcile net payroll deposits against gross calculations, and ensure all transactions sync to your accounting software. Each handoff between systems introduces error risk.

Fee duplication occurs when separate vendors each charge platform fees, PCI compliance fees, monthly minimums, and ACH transaction fees. A business paying $49/month for merchant services plus $39/month for payroll software plus separate per-transaction fees on both platforms pays more than the equivalent integrated solution that bundles these costs.

Key Takeaway: Separate merchant services and payroll systems create data fragmentation requiring manual reconciliation, add 5 to 10 hours of monthly administrative work, and duplicate platform fees, PCI compliance charges, and ACH costs — inefficiencies that an integrated platform eliminates.

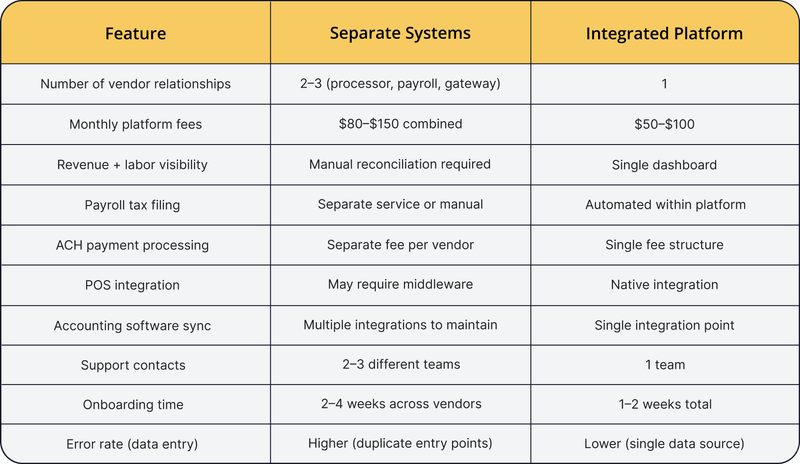

Feature Comparison: Separate vs. Integrated Platforms

The following comparison maps the operational experience across both models for a small business processing $75,000/month in card transactions with 15 employees.

The integrated model's efficiency advantage grows proportionally with business complexity. A single-location retail business saves hours. A multi-location operation with shift-based employees and high transaction volume saves days.

Key Takeaway: Integrated payment and payroll platforms reduce monthly fees by 20% to 35%, provide single-dashboard revenue and labor visibility, eliminate multi-vendor reconciliation, and cut onboarding from 2 to 4 weeks to 1 to 2 weeks — with efficiency gains scaling proportionally for multi-location businesses.

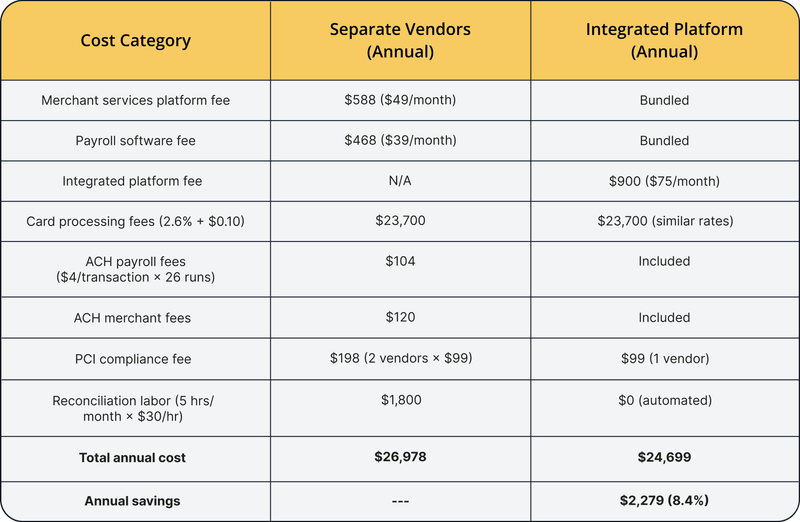

Cost Savings Example

The following scenario compares annual costs for a small business ($75,000/month in card transactions, 15 employees, bi-weekly payroll) using separate vendors versus an integrated platform.

The $2,279 in direct cost savings does not account for the value of 60 hours annually recaptured from reconciliation work — time your team can redirect to revenue-generating activities. At $30/hour, those recaptured hours represent an additional $1,800 in productivity value, bringing total annual benefit to over $4,000.

Key Takeaway: A small business processing $75,000/month with 15 employees saves approximately $2,279 in direct costs (8.4%) and recaptures 60 hours of annual reconciliation labor ($1,800 value) by switching from separate vendor systems to an integrated merchant services and payroll platform.

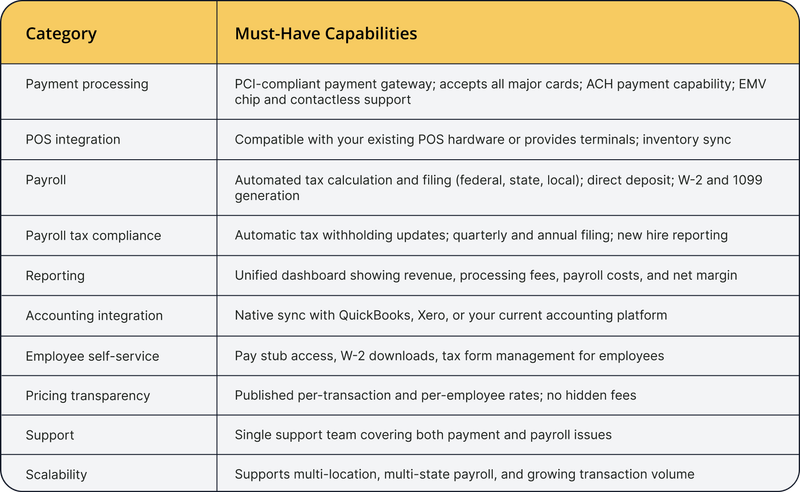

Integration Checklist: What to Evaluate

Selecting a unified payment solutions platform requires evaluating both the payment processing and payroll capabilities to ensure neither function is compromised for the sake of bundling. Use this checklist to assess platform readiness.

Platforms that excel at payment processing but offer payroll as an afterthought — or vice versa — create the same fragmentation problems as separate vendors, just with a single login screen. Evaluate each function independently before assessing the integration benefits.

Key Takeaway: Evaluate integrated merchant payroll platforms against 10 categories including PCI-compliant payment processing, automated payroll tax compliance, unified reporting dashboards, native accounting software sync, and transparent per-transaction and per-employee pricing — ensuring both payment and payroll functions are fully capable, not afterthought add-ons.

Frequently Asked Questions

Can you combine merchant services and payroll?

Multiple platforms now offer combined merchant services and payroll as a single, unified solution. These all-in-one platforms process card transactions, manage direct deposit payroll, handle tax withholding and filing, and provide consolidated reporting through one dashboard.

What is the best all-in-one payment and payroll system?

The best system depends on your transaction volume, employee count, and POS requirements. Prioritize platforms with strong capabilities in both payment processing and payroll — not one with the other bolted on. We help small businesses evaluate and implement unified payment solutions sized to their operations.

How do integrated payment systems save money?

Integrated systems save money through eliminated duplicate platform fees (20% to 35% reduction), removed reconciliation labor (5 to 10 hours/month), consolidated PCI compliance charges, and bundled ACH fees. Total annual savings for a typical small business range from $2,000 to $5,000.

What should small businesses look for in a payment processor?

Look for PCI compliance, transparent pricing without hidden fees, ACH payment capability, POS hardware compatibility, accounting software integration, and responsive support. If combining with payroll, verify that automated tax filing, direct deposit, and W-2/1099 generation are fully functional — not limited add-on features.

Is it better to use one provider for payroll and payments?

For most small businesses, a single provider reduces costs, eliminates reconciliation, and simplifies operations. The exception: businesses with highly specialized payroll needs (union, multi-state, complex commission structures) may need a dedicated payroll platform alongside their merchant services until integrated platforms mature in those areas.

Simplify Your Operations With One Platform

Combined merchant services and payroll eliminates the administrative overhead of managing separate vendors while reducing total costs by 8% to 15% for typical small businesses. The efficiency gain compounds monthly as reconciliation hours disappear, fee duplication ends, and your team accesses revenue and labor data from a single dashboard.

We specialize in unified payment solutions for small businesses that value simplicity without sacrificing capability. Contact us to receive a customized cost comparison for your business and see how much time and money integration can save.

Subscribe to our blog

Get more great articles just like this one delivered straight to your inbox.

Thank you for for submission! We will get in touch with you shortly.

Real people. Real support.

Connect with a human and get all your questions answered. Our team members are standing by.

Simple, guided setup.

Customer care you can rely on.